Inflation Reports, Hikes, and Interventions

Inflation Reports, Hikes, and Interventions

Last 2 Weeks in $Macro Twitter.

This is a Truflation’s weekly (and sometimes biweekly) newsletter. We try to recap the most important events, stats, charts, and voices in macro every week. But last week we’ve been busy so here’s a short 2-week recap.

In this episode, we’ll cover the following:

The BoJ Intervention

The UK Govt Reshuffle

Since the sacking of the UK’s finance minister, Kwasi Kwarteng, and the new Chancellor of the Exchequer, Jeremy Hunt, reversing almost all new policies of Liz Truss, the UK bond markets dropped from their 4.7% and 4.8% to an almost comfortable 3.9-4.3%.

The gilts stayed relatively stable despite PM Liz Truss being forced to resign just after 44 days in office and general mayhem in the UK government, as the Conservative Party began searching for a new leader, yet again.

Liz Truss resigned in an official speech, where she stayed defiant and unapologetic about her policies.

SkyNews comedy stunt on whether lettuce would outlive the PM paid off, and the ‘Lettuce Liz’ celebrated a victory.

The lettuce costume was a real winner this Halloween.

Immediately after Friday’s news that PM Truss would resign after a vote of no confidence, Boris Johnson flew back to the UK, with many expecting him to go against Rushi Sunak for the party leader and a PM position.

Backers and media quoted anonymous sources claiming he secured the necessary 100 MP votes of support.

During the weekend, everything was still in the air for Johnson, Sunak, and a third candidate, Penny Mordaunt.

Despite many rumors that Boris Johnson would attempt to take over once again, he backed late on Sunday, with some saying he didn’t actually get the required 100 votes of support from his MPs.

The only other opponent, Penny Mordaunt, pulled out on Monday after not getting the 100 MP quorum.

And Rushi Sunak took over on Tuesday and went off to meet the king.

Praises of PM Sunak included him being the youngest and also the first UK PM of color and a Hindu, and his wide support in the party, including from Jeremy Hunt (the new Chancellor).

Criticism included the fact that Rushi was the Chancellor of the Exchequer during Boris Johnson’s government, which led to the decisions that caused the current widespread Cost-of-Living crisis.

Him not being elected in the general elections and a 3rd candidate of the currently ruling conservative party after Boris Johnson and Liz Truss. Rushi also participated in the infamous party happening during the Covid lockdowns that got Boris fired.

His high net worth and alleged Russian affiliation through his father-in-law.

And the state poor of his own constituency region.

On conspiracy theory front, some suggested that the bankers orchestrated the bond shutdown to stage a coup in favor of their preferred candidate, Rushi Sunak.

While others laughed that all 3 Tory candidates had links to the WEF.

Either way, Tuesday, Oct 25, Rushi Sunak began by reappointing many controversial ministers from Johnson’s and Truss’ governments to form his own.

He also warned of the tough decisions ahead.

Spelling austerity and tough stance on immigration.

He also immediately rejected the idea of general elections, and the speed at which the Tories chose the new PM seemed to have helped squash the voices of the opposition in the matter.

Despite the political chaos, markets seemed to react favorably to promises of austerity, and the bond yields remained near the manageable 4% levels, far lower than during the Kwarteng-Truss ordeal.

UK Inflation

The markets weren’t even deterred by the double-digit’s inflation in the UK, announced by the Office of National Statistics (ONS) on Oct 19, 2022.

According to the ONS, the price indexes for food in the UK were especially high in September, while the lower gasoline prices were a downward contribution.

The Financial Times noted that food and non-alcoholic beverages might have risen by 14.6% in September, quite a steep number in itself. But some important staple foods like bread and pasta increased by more than 30%.

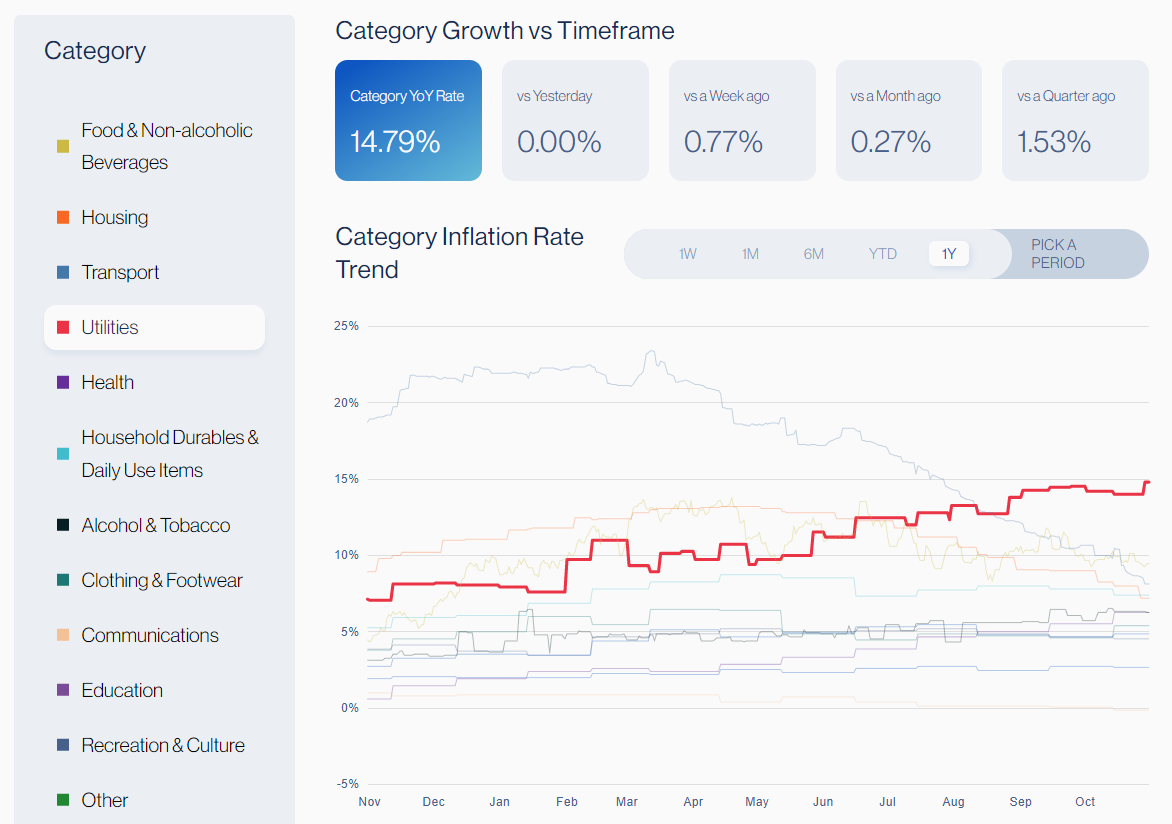

Truflation’s data suggested that UK inflation was 17.3% on the 19th of October, and the biggest contributing indexes were related the housing and utilities. Our daily index varied between 15.2%-16.5% across September 2022. You can see examine our daily numbers on the Truflation dashboard.

BoE QT

After the bond market seemingly stabilized since Jeremy Hunt became the chancellor, the BoE reasserted its stance on not prolonging the bond purchases.

BoE claimed to have worked closely with the UK Pension Funds and that they are now much better prepared for the bond market volatility.

The BoE did demand reimbursement of the 11 billion pounds ($12.4 billion) out of the 19 billion pounds ($20 billion) spent on the gilt’s purchases, from the Treasury (aka people’s taxes).

Oct 19, BoE announced it would start selling bonds in the QT operation on Nov 1. The Central Bank wants to reduce its balance sheet by selling short and medium-maturity bonds.

So, we’re up for an interesting 1st week of November between the UK bonds and the US FOMC meeting.

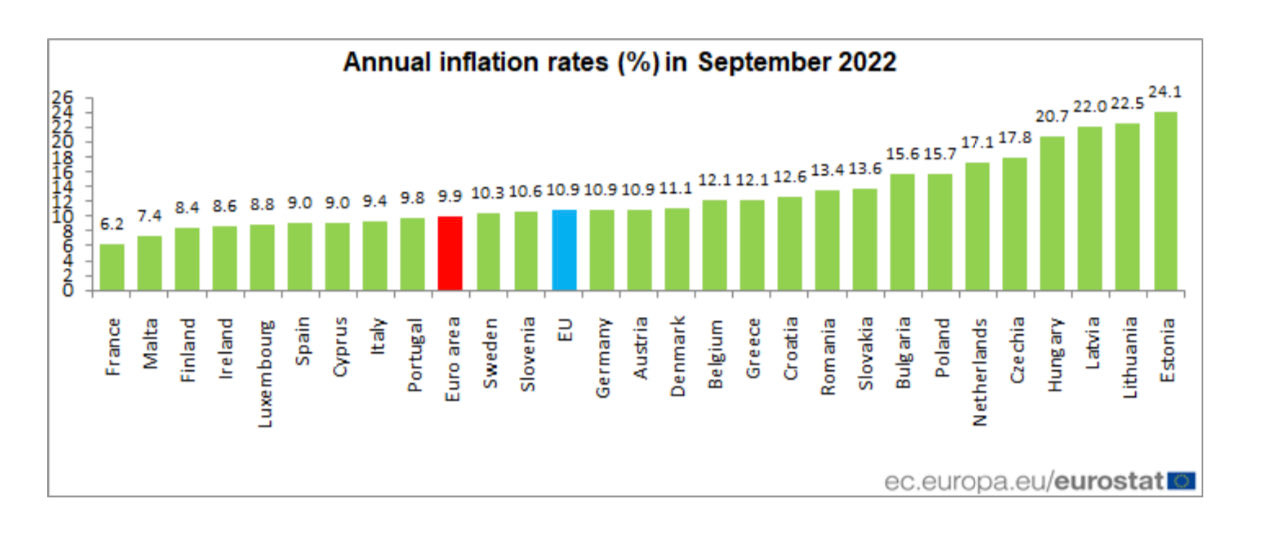

Inflation in Europe

Inflation in Europe increased to double digits at 10.9% in the EU and 9.9% in the Euro area, with many countries with inflation above 10%.

The numbers put a question mark on the hopes of the ECB pivot toward looser policies.

The ECB decided on a 0.75% interest rates hike as expected, yet the markets read some dovishness in the fact that the vote was not unanimous.

ECB might be planning more ‘triple’ hikes next month.

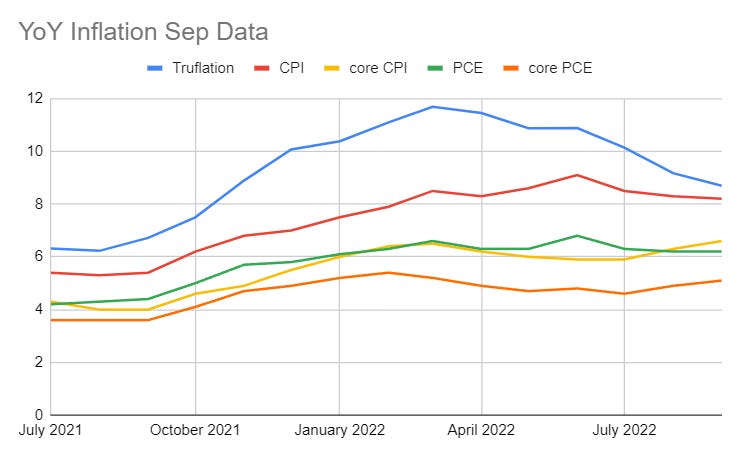

US Inflation (PCE)

The Fed’s favorite index, the core PCE, increased in September.

PCE indexes remained flatter than CPI indexes, and both flatter still compared to the Truflation index, which follows commercial price indexes for rent, cars and other items, which tend to fluctuate more than the government metrics for the same categories.

According to Truflation, the headline inflation that includes food and energy kept dropping since September and is currently below the government metrics at 7.6%.

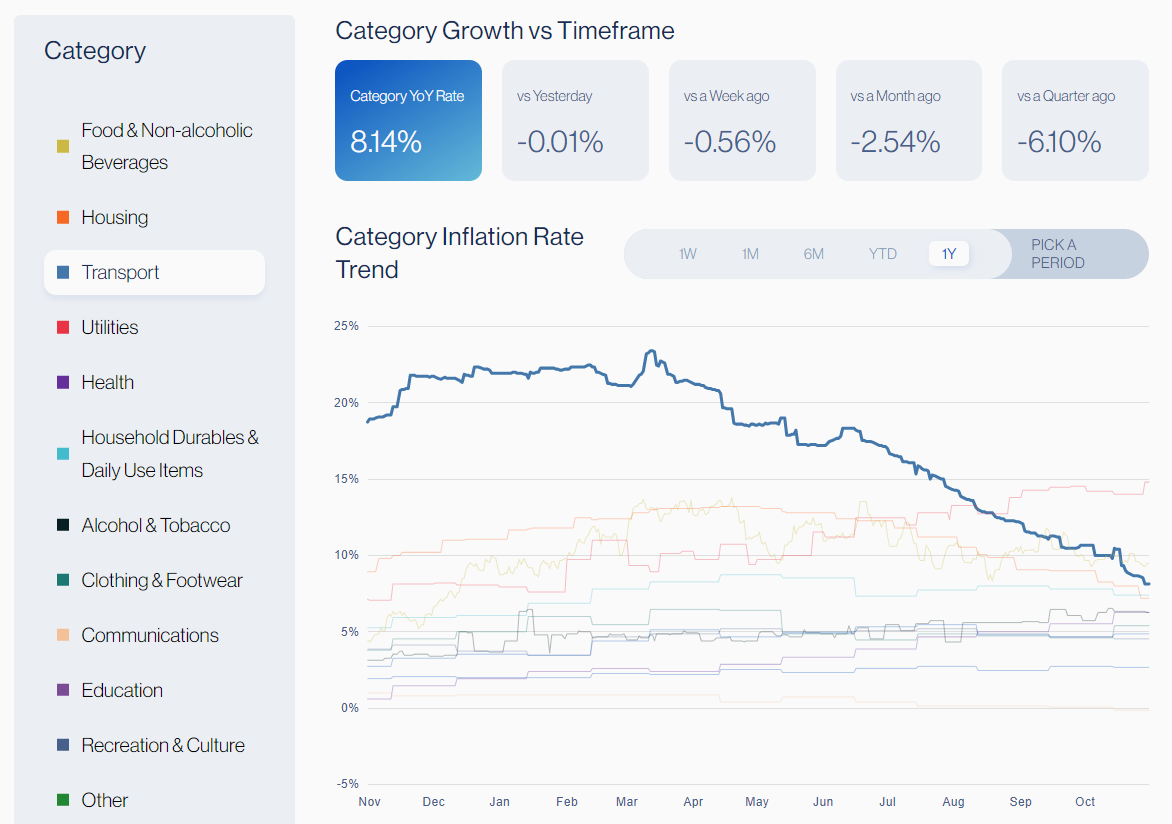

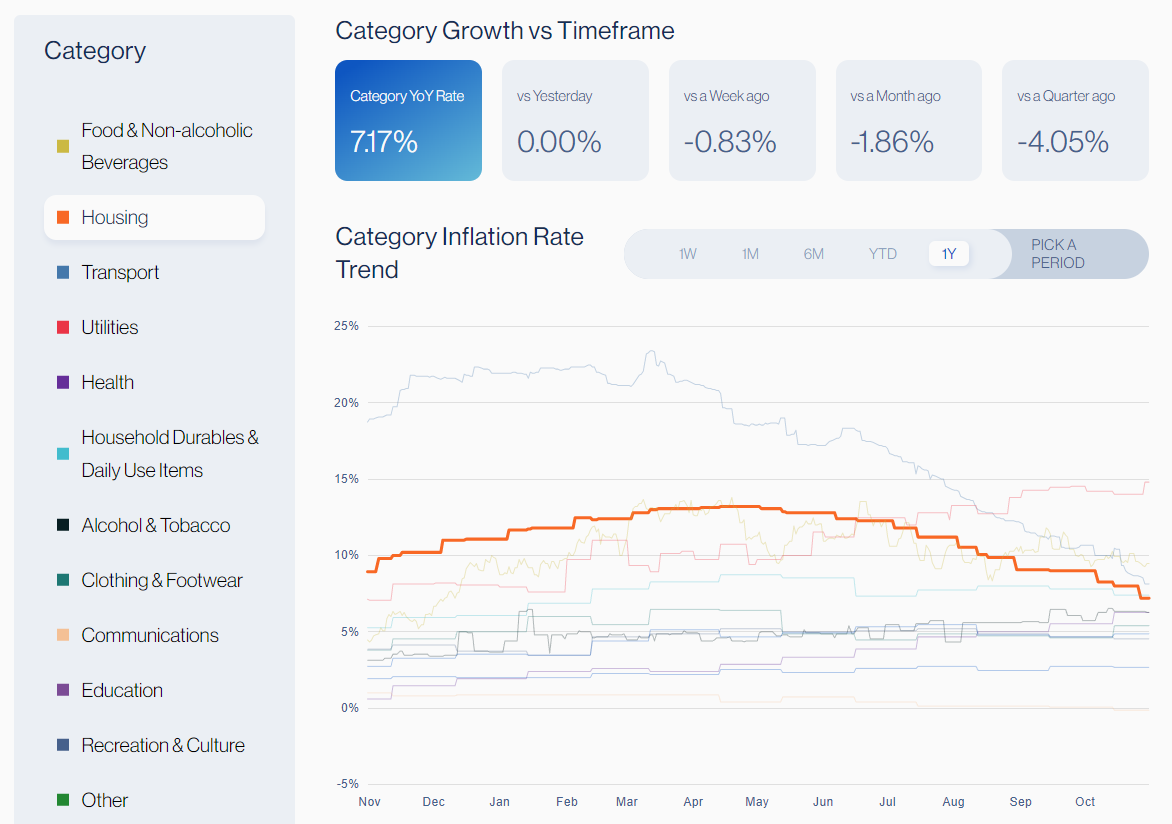

The main indexes that contributed to that drop were:

Transport (mainly used cars, but also new cars and gasoline).

Similar to commercial indexes like Manheim

Housing

Similar to Zillow

At the same time, according to our data, utility prices increased:

As did the medical costs (aligned with the findings of the GDP report from the BEA, Oct 27, 2022)

US GDP

US GDP came out positive in Q3 and higher than expected at 2.4%. It’s the first estimate out of 3 and will still be revised, but it seems the US has avoided a recession, for now.

The positive numbers come mainly from exports (trade) that included the sales of oil from the SPR (Strategic Petroleum Reserves) and weapons by the Biden administration.

Consumer spending seemed strong, but mainly due to higher prices of services, especially in health care. Consumer spending on goods decreased. Despite the strong dollar, which should have made importing goods much cheaper, the imports decreased in the US in September, also adding to the higher GDP.

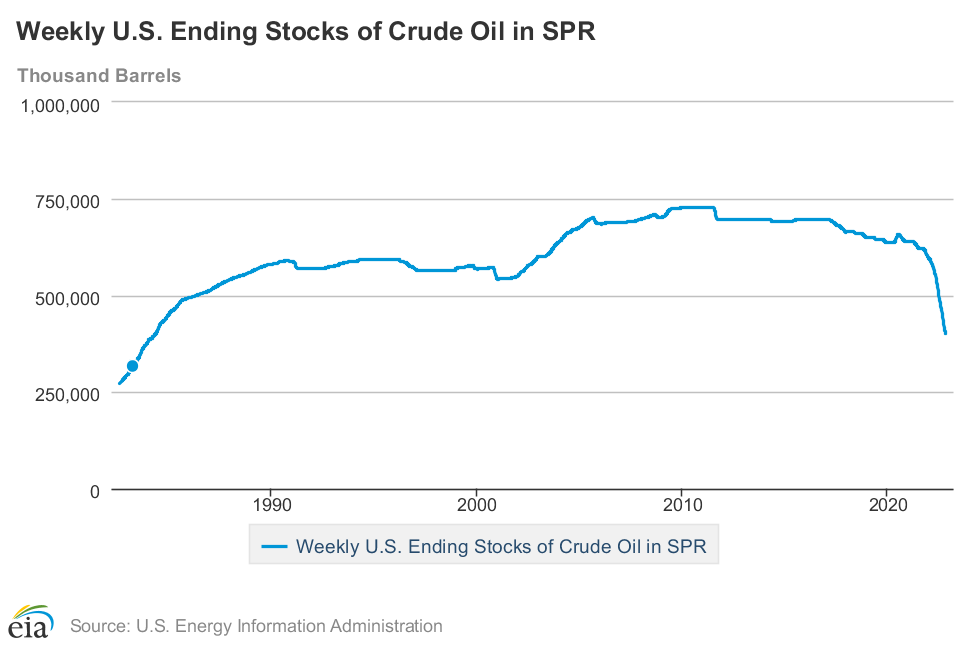

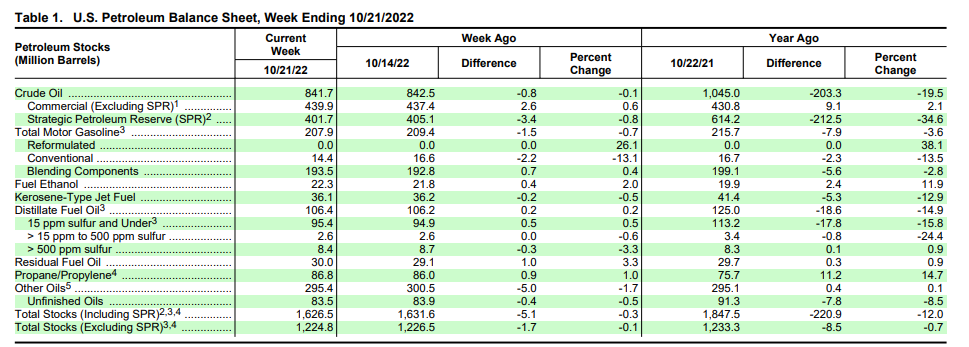

US SPR

On Oct 21, the EIA announced that the Strategic Petroleum reserves are now at a 40-year low. The US has ~402 million barrels left, which is -34.6% or -212 million barrels less than last year and -325 million barrels lower than the SPR record of 727 million barrels (2009).

Last week, President Biden announced a sale of another 15 million barrels.

Promising that he’ll refill the SPR at $67-72 per barrel.

He also urged domestic companies to produce more oil and lower their profit margins while America is at war after Shell doubled its profits in Q3. The US currently produces 12 million barrels per day, but it uses 20 million.

However, domestic companies don’t want to invest more in expanding their infrastructure for a few months or even years when their industry is bashed by the administration and actively being replaced by green alternatives.

Biden also offered domestic companies $70 per barrel, way below the market price, while OPEC was offered $80, after which it decreased production by 2 million, which we covered in our OPEC newsletter.

Both domestic companies and Saudi Arabia commented unfavorably on the US (and other countries) releasing their oil reserves to manipulate the prices in the short term. It is rumored to be one of the reasons that OPEC+ agreed to cut their production ceiling.

President Biden also bragged about lowering gasoline prices either by pointing to changes counted since June, not showing the full picture,

Or by outright stating wrong numbers in his recent speech.

Republicans promised to launch an investigation into what they consider excessive use of the Strategic Petroleum Reserves.

In another development, Mansfield Energy company warned the public about the impending diesel shortages in the Southeast due to “poor pipeline shipping economics and historically low diesel inventories.” States expected to experience serious shortages include Maryland, Virginia, Alabama, Georgia, Tennessee, North Carolina, and South Carolina.

BoJ Intervention

In the last few weeks, the Japanese Yen lost lots of ground to the strengthening dollar, prompting the BoJ to do Quantitative Easing.

It’s not the first time BoJ intervened in the past weeks.

The latest intervention was considered massive

But not as effective as expected.

It also seems that Janet Yellen, the Secretary of the US Treasury, might not have known about the BoJ decisions,

while the Japan’s minister claimed they were coordinated with the US.

The BoJ actions renewed the ‘Fed pivot’ narratives as the global markets await another FOMC meeting beginning of November to find out how much the Fed will hike its rates.

Written by Natalia Nowakowska

Excellent recap as usual. Thanks!

Being loving the style of your newsletter. The bundle of different Twitter accounts focusing on the same theme plus the data you show is a good idea.

Simple, fast and visual. Keep the good work!