Nobels, CPIs, Reversals, & U-turns

Nobels, CPIs, Reversals, & U-turns

The week in macro voices

Last week was full of unexpected news.

Nobels

Monday, Oct 10, started with an announcement that Ben Bernanke (and two others) got a Nobel Prize in Economics for his 1980s research into the financial crisis, especially Great Depression.

Bernanke challenged the previous consensus that financial crises caused the run on banks and replaced it with a new paradigm embraced by today’s central banks that the bank runs cause crises.

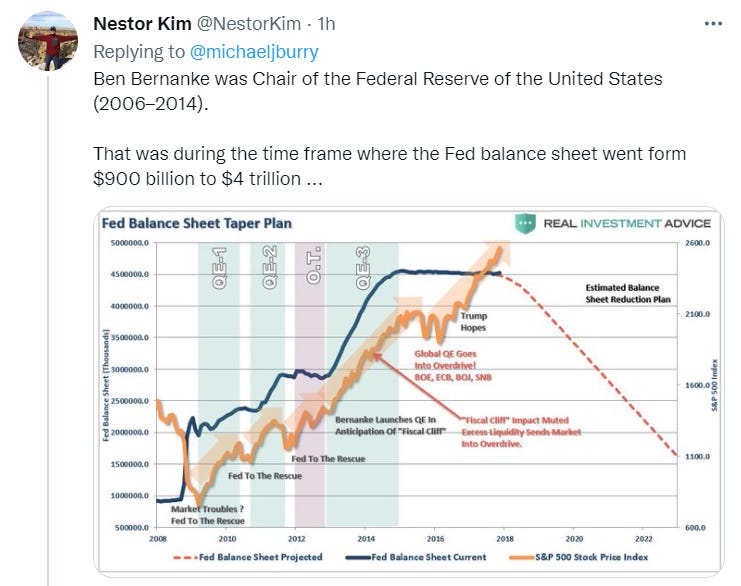

The Nobel announcement was met with criticism because Ben Bernanke was a Chair of the Federal Reserve from 2006 to 2014 during the financial crisis of 2007-2009 and introduced and advocated the massive and controversial QE and bank bailouts.

The surprising award was ridiculed by Michael Burry, who predicted the housing collapse years before anyone.

Ben Bernanke is also the man behind the Fed’s policy of expanding its balance sheet, which many analysts consider a real reason behind the affordability crisis, wealth gap, asset inflation, and subsequent consumer inflation, among others.

His actions, which likely saved the financial institutions in 2008, also became a permanent loose monetary policy going forward.

Gilts

The British bond markets, called gilts, continued to deteriorate this week as the UK government and BoE scrambled to make last-minute decisions to stabilize the situation.

Ahead of the markets opening on Monday, the Bank of England announced that it would double the ceiling for UK bond purchases from 5 billion to 10 billion pounds.

The markets didn’t believe the BoE, especially after the bank only purchased 850 million out of a potential 10 billion pounds worth of bonds on Monday.

And the bond yields edged back closer to the 5% threshold.

The BoE also reaffirmed that the unprecedented bond purchases would end by Friday, Oct 14, as previously announced.

On Tuesday, the Governor of BoE, Andrew Bailey, emphasized that gilt purchases were a financial stability intervention and repeated that the pension funds have only 3 days to get their things in order.

Bailey’s statement toppled the gilts again, wiping the BoE efforts and billions of pounds used to stabilize the markets.

The UK U-turn

In another surprising twist, Thursday, the UK Chancellor got called back early from his meeting at the IMF.

The rumors about the Chancellor getting sacked turned out to be true.

On Friday, the UK PM Truss announced the new Chancellor, Jeremy Hunt, and reversed her plans to scrap tax increases for big corporations meaning the taxes will rise as initially planned by Boris Johnson from 19% to 25%.

The abrupt decision that many Britts have called for didn’t help to stabilize the pound prices

or the bond markets.

Bonds

While gilts re-broke despite the BoE actions,

All global bond markets also suffered further losses and yield increases this week.

Experiencing high volatility

And low liquidity.

In effect, the US Treasury asked major banks whether it should buy back bonds to increase liquidity. If it does, it might be considered a QE pivot, BoE-style.

PPI, CPI, and inflation expectations.

This week was rich in inflation data releases.

Inflation Expectations

Consumer Expectations are the forward-looking metrics that the Fed officials often look at to see if inflation got ‘entrenched.‘

This week, the Michigan 1-year inflation expectations jumped to 5.1% from 4.7%. Michigan’s 5-year inflation expectations increased to 2.9% from 2.7%.

While the NY Fed inflation expectations decreased for the 1-year but increased for the 3-year and 5-year periods.

Producer Price Index (PPI)

The PPI came out on Oct 12, ahead of the CPI this month. The year-over-year percentage change in the producer price index for September was lower than previous month but higher than expected, fueling speculation about the upcoming CPI report.

The monthly change in the PPI was considered particularly bad, coming at +0.4% and higher than predicted.

The headline inflation (CPI) for September

On Thursday, the BLS released its monthly report about the consumer price inflation (CPI) for the preceding month, gathered through consumer and shop surveys following up to 80,000 items.

The consumer inflation report for September came hotter than expected, with the core CPI, which excludes energy and food prices, going up significantly and the headline CPI going down less than expected.

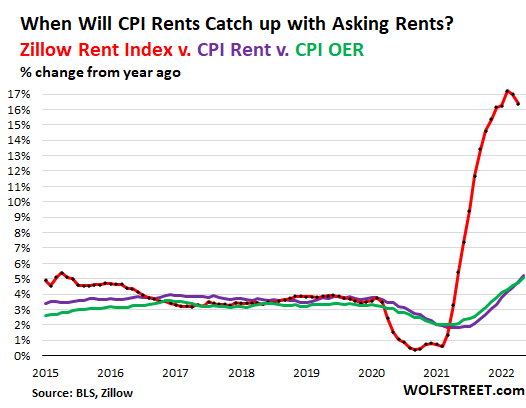

The biggest yearly price increases were still strongly related to the oil and natural gas prices expressed in gasoline, fuel oil, utilities, electricity and transportation. The lower indexes for used cars and shelter were related to the higher interest rates.

Some contrarian analysts noticed that the rents might have rolled over with the wage markets starting to cool.

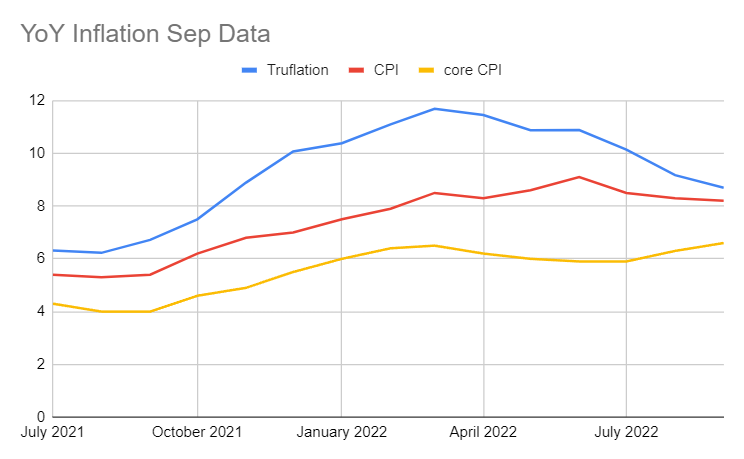

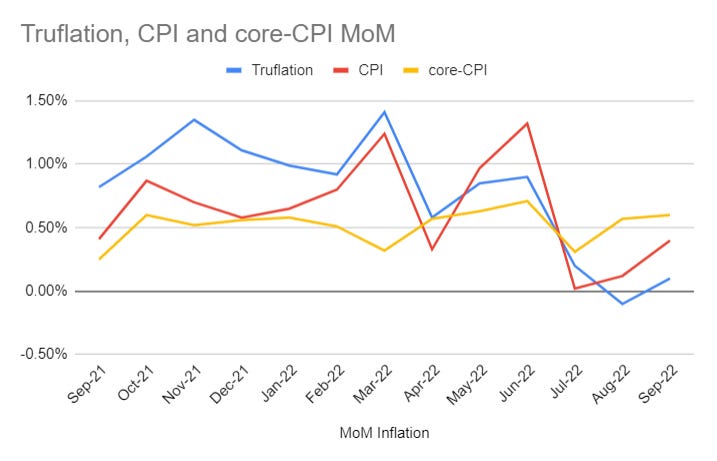

Truflation

The Truflation index kept edging down despite all the US CPI and PPI drama. It was nearing 8% in early and mid-October.

Compared to the BLS data for September, our monthly average started to come close to the official annual change in the price increase (YoY% CPI).

The monthly changes for Truflation weren’t quite as dramatic as the CPI in September, but we also saw a sudden uptick after a few months of decreases.

The post-CPI Markets

The markets reacted strongly to the headline and core CPI release wiping substantial gains off the S&P and Nasdaq.

But later in the day, the markets experienced a most dramatic reversal since 1783.

Many analysts don’t think the Fed will pivot, given that inflation is slow to drop, and the core (sticky) inflation is still rising.

Others think the Fed will have no choice but to step in, similarly to the BoJ and BoE, due to the incoming bonds market collapse and financial instability.

Deflation

Monday, Oct 10, Cathie Wood wrote an open letter to the Fed warning about deflation, a recurrent topic we previously covered, often supported on Twitter by Elon Musk.

A slew of memes followed as the ARK Invest kept bleeding money.

On a deflation front (or rather disinflation, slower price increases), this week saw a further jump in the US mortgage rates. House prices are not part of the consumer price index, but they affect the rent indexes in the longer term.

The high-interest rates made houses even more unaffordable and might soon burst the housing bubble.

The UK mortgages became more expensive than renting this week.

All the while, the market rent indexes have been coming down since the beginning of the year, unlike the indexes used by the BLS to measure CPI inflation.

The lower pace of rent inflation was also reflected in the Truflation’s housing price index for rented and owned dwellings and other lodgings, which has been going down since May 2022.

Other signals were coming from the car price deceleration. We’ve seen our YoY car price index drop since March 2022.

And according to Manheim, used car prices have been decreasing since the beginning of 2022, unlike the survey-based indexes used by the CPI to measure inflation.

The hikes in the Federal interest rates also affected car loans, making them too expensive and unaffordable in what looks like a successful attempt to curb demand. So, it’s likely we’ll see those 2 major markets tumble even if not reflected in the CPI inflation.

In other news

This week, the markets and media also continued to dissect the OPEC and Saudi Arabia situation in relation to national security. We’ve covered the underlying nuances of the OPEC and BRICS situation in our last week’s newsletter.

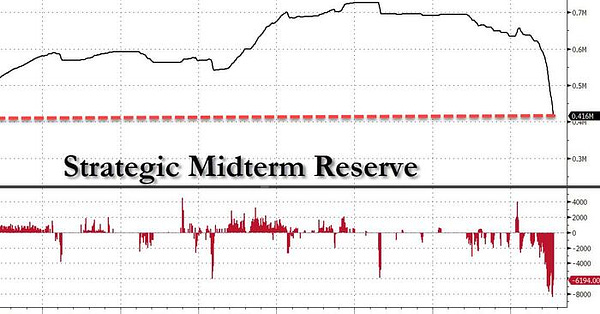

The White House reiterated that all tools are on the table to fight oil prices, including even more SPR releases. SPR is currently at a 37-year low of 416 million barrels, down from a maximum of 726 million barrels.

Also, Credit Suisse, which we covered in a previous newsletter, kept resurfacing, as the Swiss Bank is now facing a DoJ US tax probe.

Hot topics next week

Coming week, the hot topics will likely include the aftermath of the UK sacking its Chancellor of the Exchequer (aka the UK’s Minister of Finance) and the U-turn on the tax cuts with the new Chancellor Hunt already saying that some taxes will have to go up. Will those moves be able to save the UK bond market?

The situation might get worse after the UK CPI release by the statistics office ONS. Our data suggest that UK inflation keeps rising despite some measures to cap energy prices. We have not seen the UK inflation peak yet, which happened for the US inflation in March 2022.

Next week we might hear even more about the Treasury liquidity problems.

The bonds will likely remain a considerable topic. Investors are losing trust in global treasuries in an economy reliant on debt issuance. If so, the central banks might soon be forced to purchase that debt themselves, like the BoJ and BoE, or let their currencies and bond markets fall.

Written by Natalia Nowakowska

Excellent update as usual!