OPEC+, BRICS, and the Petrodollar

OPEC+, BRICS, and the Petrodollar

Recap of the macro week with the focus on oil.

Quick Macro Week Summary

Before we jump into the main topic of this week, OPEC+ and oil, a quick recap of the last Macro week.

Monday, Oct 3, FinTwit and mainstream media were still discussing the bond markets and the Credit Suisse debacle, which we covered last week.

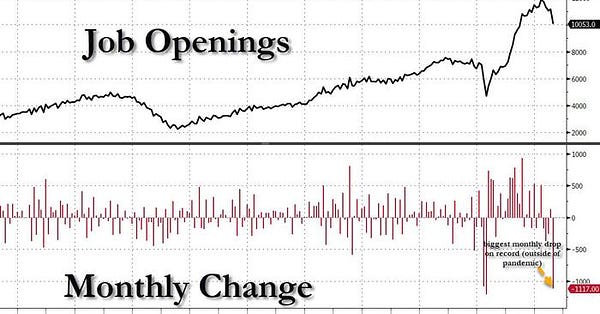

Tuesday, BLS released a job openings report, which gave the market hopes of the labor market softening with the largest drop in job openings since the lockdowns.

Wednesday, OPEC+ made a decision to cut its ceiling output by 2 million barrels per day, and the White House prepared to ease sanctions against Venezuela to let Chevron source more oil.

Thursday, the US national passed $31T trillion dollars.

Friday, the BLS released the State of Employment report, which came better than expected and caused markets to collapse on the fears of more Fed tightening. The good news is bad news again.

Credit Suisse announced $4.7 billion in bond buybacks to assure investors of their liquidity while also scrambling to sell a landmark Savoy hotel in Zurich.

And California has sent the first inflation relief checks of an estimated $9.5 billion in total.

In other news, Biden warned of a nuclear Armageddon during the Democrat fundraiser dinner. 😱

OPEC, BRICS and Petrodollar

We’ve been planning to talk about BRICS and Petrodollar for a while now, and the topic goes well with OPEC+’s recent decision and its implications, so here we go.

What are OPEC and OPEC+

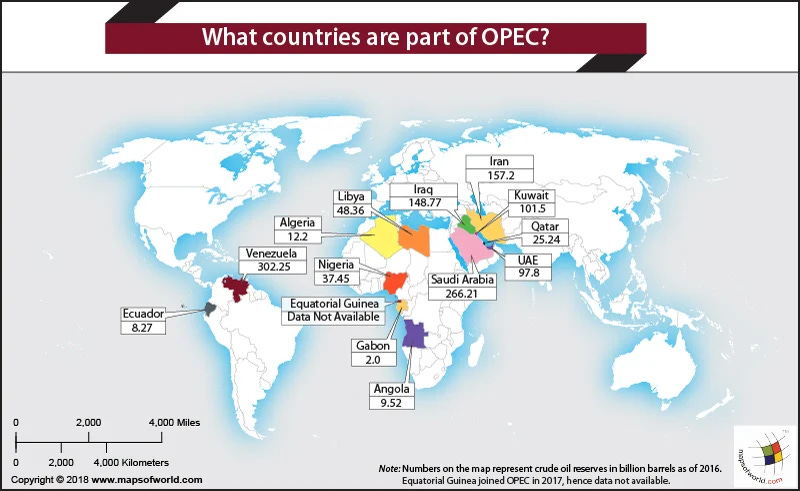

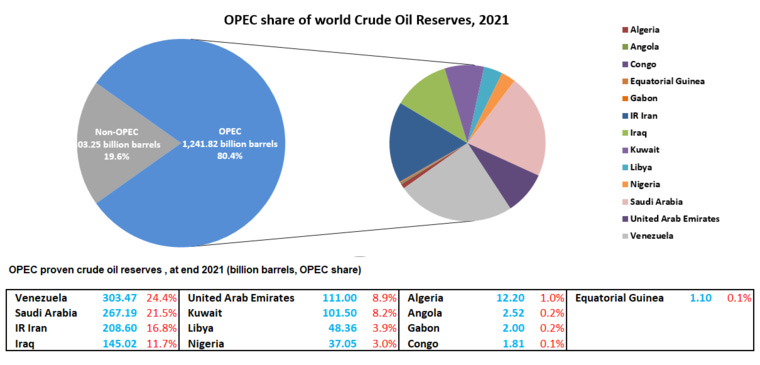

The Organization of the Petroleum Exporting Countries (OPEC) was established in the 1960s by Iran, Iraq, Kuwait, Saudi Arabia, and Venezuela. It’s a cartel consisting of 13 of the world’s major oil-exporting nations, and it can affect the price of oil by regulating the supply.

OPEC+ relates to other affiliated oil-producing countries that participate in the voluntary cuts, which include Azerbaijan, Bahrain, Brunei, Kazakhstan, Malaysia, Mexico, Oman, Philippines, Russia, Sudan and South Sudan.

OPEC+ Decision

Beginning of the week, OPEC+ signaled a willingness to cut supply by 1 million barrels a day in response to Russia’s request, which initiated the oil price hikes.

The Biden administration lobbied hard to prevent that, including promises to buy 200 million barrels of oil to replenish the depleted SPR (Strategic Petroleum Reserves). But in the end, OPEC+ decided to cut by 2 million barrels (although the decision might not have a real impact on the outputs because currently, the OPEC countries are 3 million barrels per day short of their production quota).

The White House made a statement about OPEC+’s short-sightedness, which could hurt smaller countries, and promised to “consult with Congress on additional tools and authorities to reduce OPEC’s control over energy prices.”

It also suggested that OPEC+ aligned with Russia

In response, Saudi Arabia challenged the US by raising prices for the US alone while lowering them for Europe suffering from an energy crisis.

WSJ reported the US administration’s willingness to deal with Maduro to let Venezuela export oil to the USA again.

Venezuela no longer produces much.

But it’s still sitting on 300 billion barrels of oil, the largest oil reserves in the world.

Ahead of the OPEC+ announcement and days following, the oil prices kept climbing, with many analysts predicting gasoline price hikes and higher inflation.

SPR

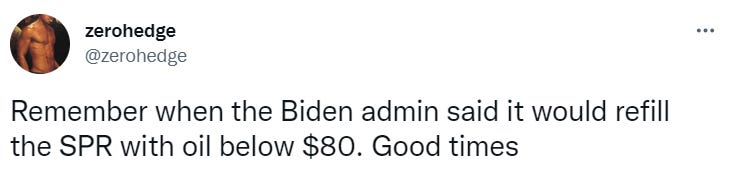

The WH response to the OPEC+ decision also mentioned a 10-million-barrel release from the SPR — Strategic Petroleum Reserves (part of the 180 million barrels approved in March 2022).

Altogether, the President approved a release of 260 barrels since November 2021, putting the reserves at the lowest since the early 80s.

The administration planned to repurchase oil at the price of around $80 per barrel; the plan was curtailed by the OPEC+ decision putting the oil prices back into the $90-100 per barrel range.

OPEC+ rejected the WH proposal to not cut output in exchange for the US making an order for 200 million barrels of oil.

Some pointed it could be a deliberate action to let the US further deplete its SPR ahead of the elections.

Many also questioned whether the US is depleting the SPR to keep inflation artificially down ahead of the midterms.

SPR releases lowered inflation at home but also put the US in a vulnerable position while it’s tackling adversaries on all fronts.

Petrodollar

The petrodollar is not a currency but a term referring to the use of the USD in all oil transactions. Thanks to the role of the status of the USD as a global reserve currency utilized worldwide, and various agreements between the US and major oil producers (OPEC countries), the dollar is used to denominate and purchase crude oil.

But it’s not just the currency that’s crucial here. Through various additional contracts, the OPEC countries agree to recycle petrodollars meaning they reinvest their oil revenues into the US economy by purchasing US treasury bonds, US arms and equipment, or investing in their development and infrastructure with US support. The petrodollar recycling maintains demand for the USD and props up the US economy.

The petrodollar is de facto the new fiat standard after the gold standard collapsed in 1971 and the 1974 agreements with Saudi Arabia about petrodollar recycling. The USD is now backed by oil and its army rather than gold and hard assets.

But Saudi Arabia has been getting rid of the US treasuries alongside other global central banks and hasn’t been petrodollar recycling since 2020.

The share of revenue that the countries hold in foreign reserve currencies has fallen steadily. The share of the reserves held by global CBs in the USD has reached its lowest in 2021 at 58.8% and is currently at 59.5%.

BRICS

That’s where the BRICS comes in, as a real threat to the petrodollar and the USD status as a global reserve currency. BRICS stands for the economic alliance between Brazil, Russia, India, China, and South Africa.

Since banning Russia from SWIFT, the Russian ruble has quickly recovered and even gained strength against the dollar.

Russia and China agreed on oil trade in Chinese yuan and Russian rubles, 50-50.

Argentina and Iran both officially applied to join BRICS (Iran being another large oil producer tired of the US sanctions).

Most importantly, BRICS countries are considering introducing a common currency based on a basket of their currencies for trade and perhaps oil trade as well. They are also amassing gold and hard assets.

Additionally, Saudi Arabia has been considering using yuan to trade oil with the BRICS countries at least since March 2022, as reported by WSJ.

If the USD seizes being the global reserve currency, printing away the massive $31 trillion of national debt and selling US treasuries around the world is going to be much harder, likely leading to a default.

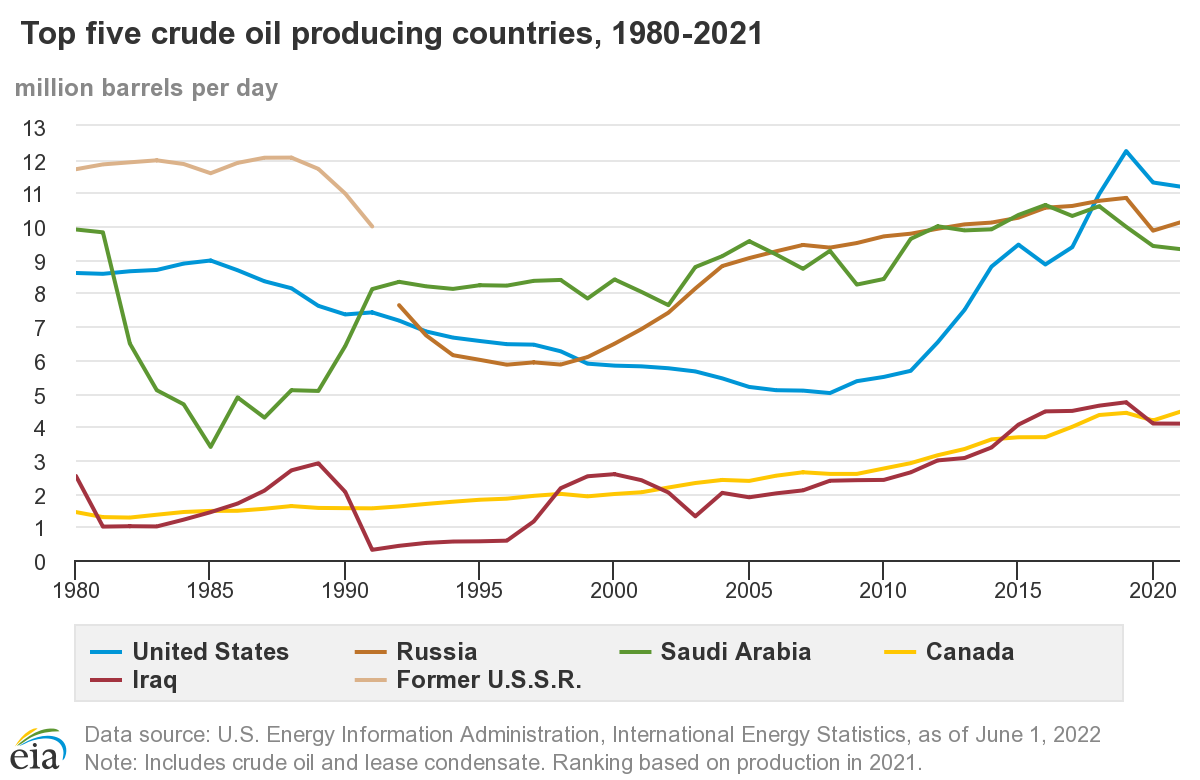

US Production

All the while, the US is the biggest global producer of oil, producing >11 million barrels per day, but currently using ~20 million barrels per day as well.

If put against the wall, the US could increase its production capacity and become independent from OPEC.

However, there are climate concerns. The administrating is hoping to solve the energy crisis within 10 years by boosting investments in renewables through the recent ‘Inflation Reduction Act’.

Hot topics next week

Another intense week ahead.

The UK bonds are preparing for a rematch despite BoE purchasing efforts.

Everyone is still watching Credit Suisse closely since its buyback liquidity might be coming directly from the Fed’s Swap Line.

The US markets are running out of liquidity.

While the debt refinancing costs are skyrocketing due to global interest rate hikes.

And the markets await the Thursday, Oct 13, CPI inflation and real wages report from the BLS to place further bets on what the Fed will do next.

Our inflation index kept dropping from August to September, driven initially by gasoline prices, but since July, also car sales prices and rent prices, while the utilities and health costs kept climbing. The Truflation index is now lower by at least 1% than last month. More info available on our free public dashboard.

Written by Natalia Nowakowska

Excellent update. Thanks!