FOMC, Inflation and 'Wen Pivot'

FOMC, Inflation and 'Wen Pivot'

What Jerome Powell tells us about the next interest rate hikes.

This is Truflation’s newsletter, where we recap some of the important events, data, and voices in macro and the markets.

In this episode, we’ll cover the following:

Last weeks the markets lived with a hope of the 'Fed Pivot' once again, while the Fed officials were unable to provide any indication due to the standard FOMC media blackout.

Banks, analysts, and media jumped in to fill the void:

Bloomberg covered Morgan Stanley's strategist, Michael Wilson, who suggested there would be "a Fed pivot sooner rather than later."

Wilson and other analysts pointed to the yield curve inversion between 10-year and three-month Treasuries, a reliable recession indicator.

The inversion of the Fed’s preferred yield curve fueled a lot of Pivot narratives ahead of the FOMC.

It added to the yield inversion of the 10-year and 2-year Treasury bonds, another important recession indicator that happened in July 2022, reaching the worst numbers since 2000.

Blackrock told its investors to anticipate a "pivot language" after the FOMC meeting.

All that, plus the ambiguous Tweets and WSJ articles by Nick Timiraos, were enough to send the markets into mini rallies ahead of the Federal Open Market Committee deliberations. WSJ Nick is sometimes called "Nicky Leaks" and is considered the unofficial Fed spokesman during the FOMC blackouts.

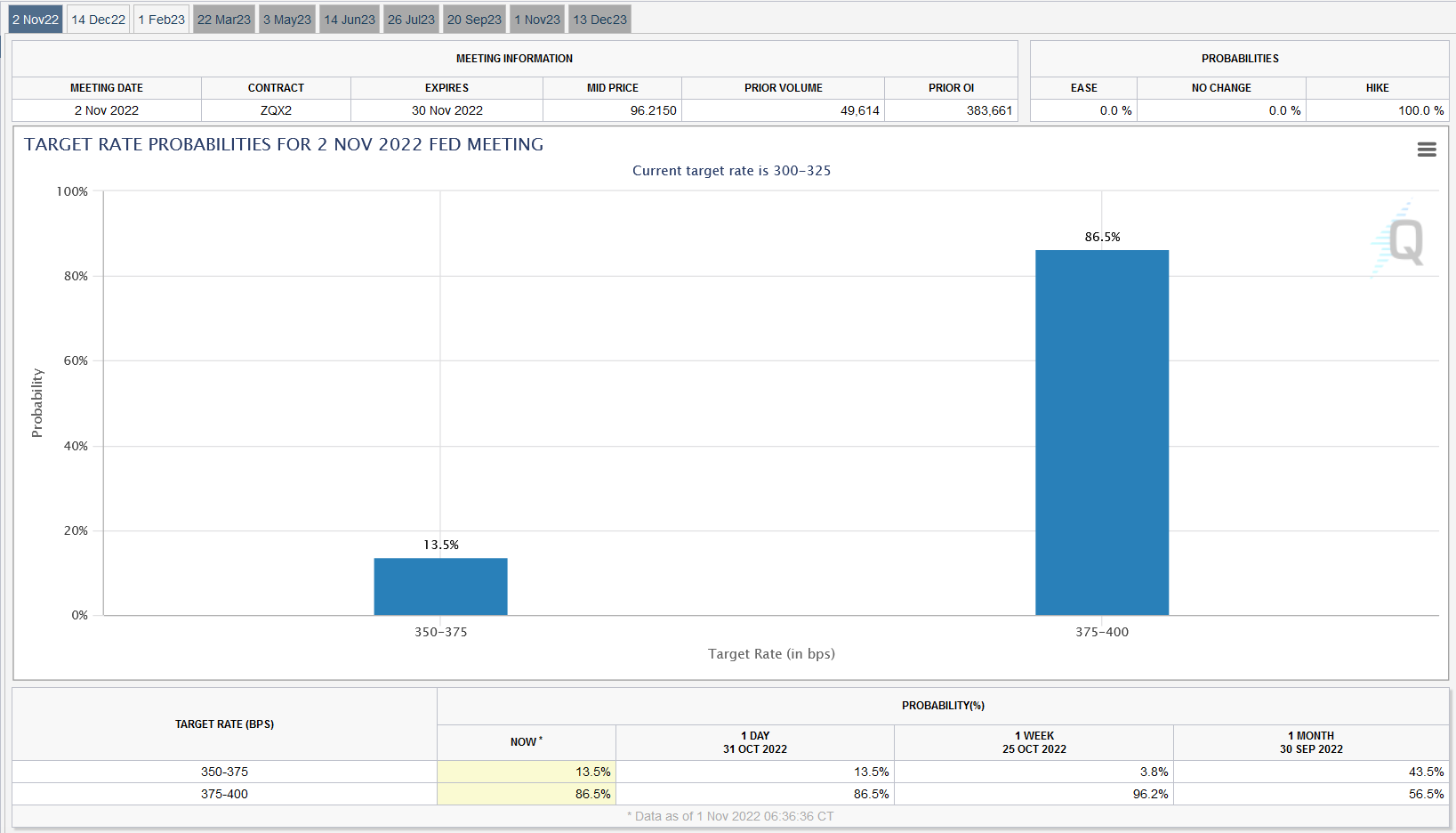

The November FOMC Meeting

On Nov 2, 2022, the FOMC made the 4th consecutive 0.75% rise (75bps), and the 6th rise in total, bringing the federal funds rate to a 3.75-4% range.

The 75bps hike towards the 375-400bps range was clearly communicated and largely anticipated by the markets.

Some markets didn’t react.

While the stocks rallied on the PR release and then crashed during the media Q&A.

Jerome’s Powell Q&A cost the markets $56 billion.

As many analysts noticed yet again, free markets should not be so dependent on the Central Banks’ policies and cheap money and hang on the Fed’s every word and every data release that can influence the Fed’s decisions.

Speculation and volatility were rampant with every FOMC meeting since the tightening started.

Markets closed on a red.

As the market participants dissected the FOMC press release and Jerome's Powell speech and a media Q&A, multiple new narratives emerged.

Dovish

Hawkish

Mixed

We’ve dissected the FOMC transcript and here are the sections we found interesting:

'Dovish' FOMC

"At some point, as I've said in the last two press conferences, it will become promote to slow the pace of increases to bring inflation down to our 2% goal."

The Fed will consider a slower pace of rate hikes, probably as soon as the next meeting in December 2022.

"Our decisions will depend on the totality of incoming data and implications for the outlook of activity and inflation. We will continue to make our decisions meeting by meeting (...)"

The Fed will continue to assess hikes on a meeting-by-meeting basis and analyze a wide range of current data. The data releases will remain important to gauge the Fed's next moves.

"We will take into account the cumulative tightening of monetary policy and the lags with which monetary policy affects economic activity and inflation."

The Fed will now also take into consideration wider economic metrics for the signs of cooling, but without specifying the metrics they will look at.

Hawkish FOMC

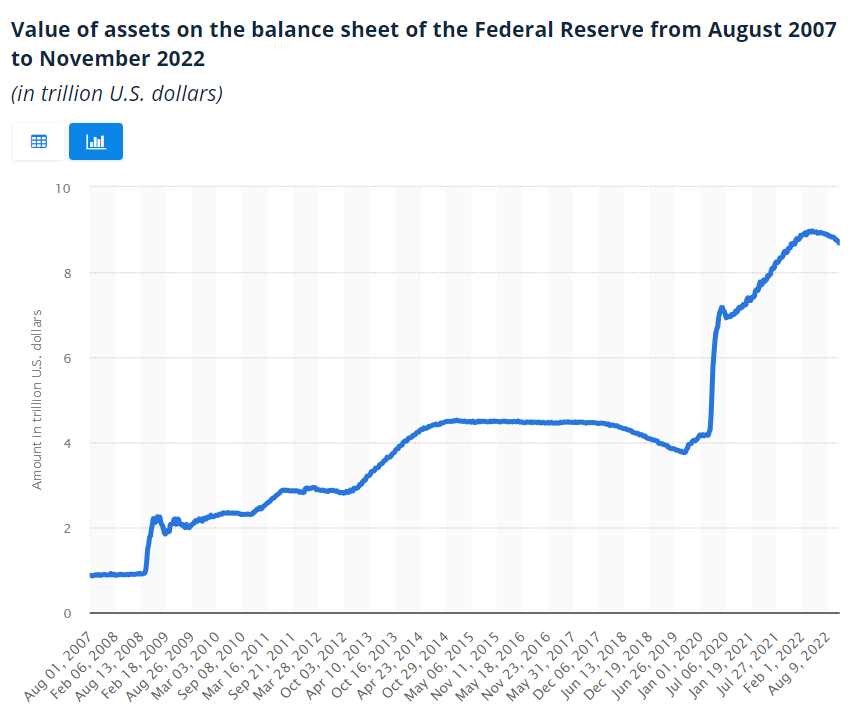

The Fed will continue "the process of significantly reducing the size of our balance sheet, which plays an important role in firming the stance of monetary policy."

We might expect some more aggressive QT.

So far, despite some promises, the Fed has been slow to shrink its balance sheet. Perhaps it will do more in this direction now. Not many analysts mentioned that point, which we find quite important.

"Incoming data since our last meeting suggests that the ultimate level of interest rates will be higher than previously expected"

The final range of interest rate hikes will likely be higher than the 4.4-4.9% predicted at the September FOMC.

"The historical record cautions strongly from loosening policy. We will stay the course until the job is done."

Historically, loosening the monetary policy too soon resulted in inflation coming back and staying for longer. The Fed will err on the side of overtightening rather than pivoting too soon.

Other

Ahead of the FOMC, many analysts, including Harvard Economics Professor Jason Furman and Economist Paul Krugman, pointed to the lagging indicators used by the BLS and BEA to calculate inflation and the rapid cooling of the commercial rent and car indexes.

The Fed’s Jerome Powell answered some of those arguments in the Q&A:

"Financial conditions have tightened significantly in response to our policy actions. We are seeing the effects on demand in the most interest rate-sensitive sectors of the economy, such as housing. It will take time for it to be realized, especially on inflation."

He suggested other market indicators capture new leases rather than existing tenants.

“I start by saying that the measure that's in the CPI and the PCE, it captures rents for all tenants, not just new leases”.

Rebuked the allegations from many market analysts and banks that the Fed is at risk or has already overtightened.

“I don't think we've overtightened. It's very difficult to make a case that our current level is too tight given that inflation still runs well above the Federal funds rate.”

On the bright side, Jerome Powell thinks that if they accidentally overtighten, the Fed can just use their ‘powerful’ covid stimmies and other helicopter money to course-correct.

“If we overtighten, then we have the ability with our tools, which are powerful, as we showed at the beginning of the pandemic episode. We can support economic activities strongly if that happens, if that's necessary. “

TLDR: This was not a pivot.

The Fed said it would continue tightening and has a way to go.

The Fed is now asking three questions: how fast, how high, and how long. It will slow, go higher and keep it high for longer.

We expect a minimum of 50 bps at the Dec FOMC.

Terminal rates might go to 5% or above until the rates are above inflation.

The Fed will keep them high until the 2% target or significant market changes.

The Fed is afraid to under-tighten. They will risk overtightening.

What metrics will the Fed look at?

This time the Fed promised it would look not only at inflation and the labor market but also at other unspecified metrics that could signal a cooling economy.

The next FOMC meeting is 13-14th December 2022. It means the Fed will look at CPI for October and perhaps November (to be released Dec 13). And a PCE for October (to be released Dec 1).

CPI inflation October

PCE inflation August

Nick Timiraos also pointed the public to ECI — Employment Cost Index, mentioned by Powell in 2021.

The Fed also looks at the

Labor data: job growth, unemployment, and wages (the bad news is good news for the Fed here).

Forward-looking inflation and sentiment metrics, like Michigan indexes

Wider market indexes like GDP, export, import, freight, the bond yields charts

And sector specific metrics, i.e., for housing like the Case-Shiller index

It might also check PPI (Producer Price Index), which was just released and came out lower than expected.

What Does Truflation Data say:

In our opinion, the Fed’s tightening is working well, and they may be at risk of over-tightening into a recession. According to our independent data, the YoY inflation rate in the US has dropped from 12% in March to 8.5% at the end of September and 7.5% at the end of October. As of Nov 15, 2022, Truflation rate was 7.14%.

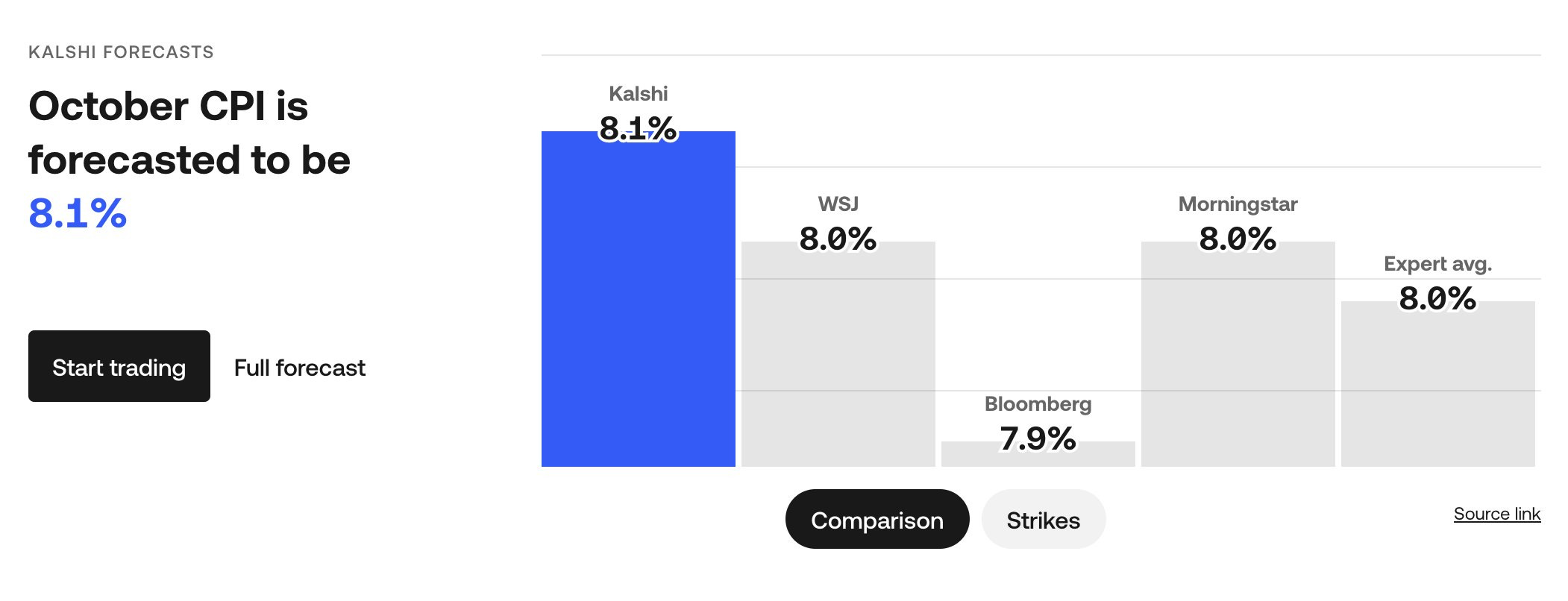

Preliminary Forecasting Models

Truflation ran two internal forecasting models using our data, which predicted the October CPI to be 7.8-7.9%, as reported in our data insights, and 7.6%, according to another unshared model.

The final CPI landed at 7.7%. Both our forecasts turned out to be more accurate than the market, banks, media, and Cleveland Fed's predictions.

‘Wen Pivot’

According to analysts, post-FOMC was the best time to buy some stocks as the markets seemingly bottomed to record lows.

The markets performed the worst in over a century. Something that gives analysts another hope for a pivot, even if the Fed insists it doesn’t care about the stocks.

Jerome Powell mentioned that the pace of the interest rate hikes might go down as soon as the next FOMC meeting in December. A sentiment recently confirmed by Waller, Daly, and other Fed officials

The markets were betting on 50 bps and 75 bps hikes 50-50 just after the FOMC meeting.

Since then, the odds moved in favor of the 50bps hikes (0.5%, as of 15 Nov).

So, if you are subscribing to the idea that Fed Pivot now means slower hikes, then it’s happening in December already.

If however, you are waiting for a pause, or better yet, hikes reversal or a QE (printer go BRRRr), you’d have to wait for a major market crash. Think black-swan-level event with mass layoffs rather than just some record lows we’re experiencing now.

The Fed already said there would be pain and showed it’s not afraid to let the markets, businesses, and the people suffer.

The Federal Reserve aims to:

“reset housing” — bring it back to affordable levels (the question is for whom)

“soften labor markers” — layoffs, unemployment, slave salaries are part of the plan to lower the demand

survive prolonged periods of “slower growth.” — negative GDP and bear market don’t scare the Fed

over- rather than undertighten — they will continue until businesses fall and recession settles in, and then they might course correct with some giveaways

Another reason for a premature Fed Pivot would be inflation quickly falling back towards 2%! Truflation data has been promising with drops of ~1% a month from the 12% peak in March. If we kept this pace, we’d be looking at 2% around Q4 2023. Here’s to hoping!

You can see our daily inflation updates on our dashboard and Twitter.

PS: We’ll try to move towards shorter and more topical updates on Substack for better readability. Stay tuned!

Written by Natalia Nowakowska

Another great update. Thanks!